The collapse of Abraaj Group may disrupt private equity businesses in the Middle East and North Africa, which have registered a decline in number of deals and exits in recent years, but the fallout may also help pave the way for greater controls that will boost investor confidence, analysts said.

“Most investors see Abraaj as a standalone issue,” said Sunaina Sinha, managing partner of UK-based Cebile Capital, which helps private equity firms find investors. “However, the story poses questions for Mena private equity, such as...what action will be taken – both against the company and its directors, and to strengthen the industry going forward?”

Abraaj, once the Middle East’s biggest buyout firm with almost $14 billion of assets under management, has faced a liquidity and reputational crisis since four investors in its $1bn healthcare vehicle alleged mismanagement of funds in February and hired investigators to find out where their money had gone.

The firm is undergoing a court-supervised restructuring and trying to sell off parts of the business to pay down an estimated $1bn of debt. According to leaks from the investigation, the company was reliant on short-term borrowing and suffered financial troubles months before the story broke. Abraaj and its founder Arif Naqvi, who is currently outside the UAE, deny any wrongdoing.

As the story unfolds, analysts say Mena private equity investing, already suffering from a lull, could be impacted further as people become more cautious. It means “more due diligence and a pause during this adjustment process”, said Richard Segal, senior analyst at Manulife Asset Management. The private equity industry in Mena was already slowing before the scandal due to macroeconomic challenges and a shift away from the high-fees business model on which it is based.

“On a macro level, private equity is booming, with allocations and exits at an all-time high in 2017 and fundraising levels strong,” said Cebile Capital’s Ms Sinha. In the first quarter of 2018, buyout firms globally had $637bn of capital available for investment, growing at an annual rate of 10.5 per cent, according to EY’s latest briefing in April.

However, the industry in the Mena region had “fallen out of favour” with investors long before Abraaj, Ms Sinha said. “People saw a lot of money going in to the region but not enough coming out. The exit record wasn’t there because, like in many emerging markets, companies were taking longer to mature and the overall return was not as great as in the US or Europe.”

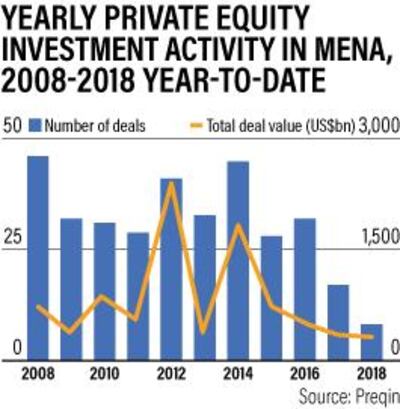

An extra layer of geopolitical risk further dissuaded some investors, she added. The number and value of PE deals in Mena has steadily declined since 2014, to 17 deals totalling $350m last year, according to figures compiled exclusively for The National by alternative assets data provider Preqin (See graph).

Between 2014 and 2015 the number and value of deals more than halved, as a sharp drop in oil prices hit the hydrocarbons-dependent economies of the Middle East, causing shockwaves across multiple industries including PE. Meanwhile, the value of exits plummeted to $52m in 2017 from $1.9bn in 2014, Preqin’s figures show.

Globally, PE investors have “fee fatigue” and many have shifted towards a cheaper, deal-by-deal approach, rather than handing a chunk of money over to a firm to spend as opportunities arise, said Firas Mallah, managing partner of alternative investment firm MMK Capital. “The rules of engagement are changing.”

Imad Ghandour, managing director of Dubai-based PE firm CedarBridge Partners and a co-founding member of the Mena Private Equity Association, told The National the industry body disbanded at the end of last year due to a declining membership base. It had 125 members at its peak in 2008 – this fell to six in 2017.

“Definitely PE managers have found it more difficult to raise funds amid slower economic growth, which affects the investment appetite of family offices and other high-net worth individuals in the region,” Mr Ghandour said. Mena private equity needs to demonstrate sustained growth from now on to reassure investors, he said.

Fethi Kirdar, chief executive of investment advisory FSK Advisors added: “We haven’t heard much about new funds being raised or committed even from the big players in the region lately, and the industry appears to be facing a tough time.”

_________________

Read more:

[ Explainer: What now for Abraaj Group? ]

[ Abraaj restructure on smoother path following bounced cheque settlement ]

[ Abraaj posts $188 million loss after using investor funds ]

_________________

GDP growth is an important driver of investment in PE and although there has been an economic uptick this year, “people have been so used to strong growth over the past 10-15 years that a slower period makes them very cautious,” he added.

Renewed economic growth on the back of higher oil prices, which are hovering at about $70 per barrel, could boost the private sector and spark higher levels of interest in PE over the coming year, said Tariq Qaqish, managing director, asset management, at Menacorp Finance. When private equity is once again yielding returns, investors may be less cautious than now and the long-term impact of situations such as Abraaj may be limited.

However, he added, “the story of Abraaj – because it was a pioneer of Mena private equity and the biggest player for so long – has damaged the industry’s reputation in the short term and the authorities must work out how to fix it, without throttling potential investment with new regulations.”

Such comments show the scale of the challenge facing regulators as they seek to manage the Abraaj crisis in a way least likely to dent investor confidence. The Dubai Financial Services Authority, regulator of the DIFC free zone where an Abraaj entity, Abraaj Capital, is registered, restricted the activities Abraaj Capital is allowed to undertake following an investigation, including stopping it from initiating new work or transferring money to other entities and affiliates. However, the DFSA has no regulatory control over Abraaj’s 19 other international operations, which fall under different jurisdictions.

Industry insiders such as Ms Sinha believe a more vocal and aggressive communication strategy by regulators helps in times of crisis.

“People want to know what happens now,” said Ms Sinha.