It was a welcome relief to many when India's central bank allowed banks to restructure some defaulting small businesses loans at the start of the year.

But the decision by the Reserve Bank of India (RBI) under its new governor, Shaktikanta Das - appointed last month following the shock resignation of his predecessor, Urjit Patel - took some by surprise.

It raised questions about whether Mr Das is caving in to the demands of prime minister Narendra Modi's government, which is eager for the RBI to adopt measures to boost economic growth – and subsequently win over voters - with a general election to be held by May, analysts say. The government was pushing the RBI last year to offer some respite to micro, small and medium-sized companies (MSMEs).

“We believe the RBI's initiative was much-required because the pain is really, really deep,” says Aditya Kanoria, director at Credent Asset Management, based in Mumbai. “The new governor is doing exactly what the government was looking forward to.”

The MSME segment accounts for almost 25 per cent of commercial lending, while employing some 120 million people, according to Indian brokerage firm Angel Broking.

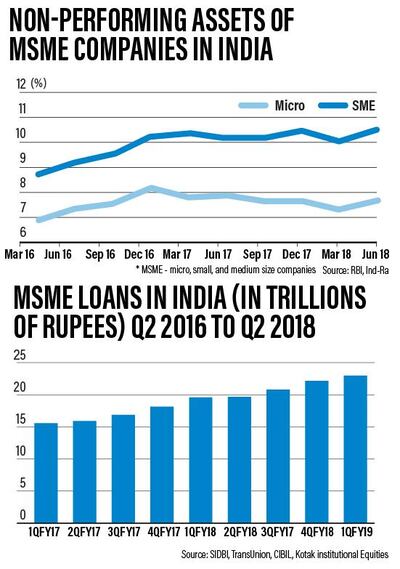

Stressed loans to small companies amount to up to 1.3 trillion rupees (Dh68.7bn), according to data from SBICAP Securities this week.

The latest RBI policy permits the one-time restructuring of loans to micro, small and medium-sized companies on liabilities of up to 250 million rupees (Dh13.2m).

“The move became necessary after credit to the MSME segment showed signs of slowing down,” says Jaikishan Parmar, a senior equity research analyst at Angel Broking.

But it came following a stormy period of relations between the central bank and New Delhi. In recent months, the RBI and Indian government have been locked in a tense public dispute; issues ranged from pressure on the central bank to release reserves to demands to ease lending restrictions on a group of public sector lenders that have struggled with bad debt. Such moves would free up the flow of credit and stimulate the economy, but it culminated in Mr Patel's resignation, who did not cede to the demands.

_________

Read more:

Behind the resignation of India's central bank governor

Indian government and RBI avert crisis but deep problems linger

Indian government and central bank fighting is bad for business

India's central banks warns government on independence

_________

GDP growth in India slowed to 7.1 per cent in the quarter to September compared to 8.2 per cent in the previous quarter.

Since Mr Das, a career bureaucrat and former economic affairs secretary, took over from Mr Patel in December, he has come under close scrutiny, as observers look for signs on whether he will uphold the autonomy of the RBI, as he stated he would, or pander to the demands of the government.

“A large number of people are under the employment of the SME sector, so if you do something good in the sector, it directly affects people who are not that privileged and that converts to votes,” says Mr Kanoria.

Small enterprises in India were hit particularly hard by the government's controversial ban on the two highest value banknotes in 2016, known as demonetisation, and the introduction of a new goods and services tax in 2017.

Banks in India have struggled with high levels of bad debt, amounting to about $150bn, according to RBI data obtained by Reuters.

A report released on Monday by the central bank, however, suggested the worst is over in terms of the non-performing assets crisis in India, with projections of banks' gross non-performing asset ratio declining from 10.8 in September last year to 10.3 per cent in March, and edging down to 10.2 per cent by September this year.

Aditya Bagree, the director of Business Aggregate, which assists traders with financing, says “we do not deny that [the general election] could be a motive to do this at this point, but all governments try to do something for various classes of the population right before the election”. He adds that while this will go some way to help the sector, there is more to be done.

Business leaders from the segment say the RBI move is a welcome step for a sector that has suffered job losses, while some cash-driven enterprises have failed to survive the impact of demonetisation and adjusting to the tech-driven GST system.

“The major recurring requirements are to pay salaries and taxes on time,” says Ritu Grover, the chief executive of TGH Lifestyle Services, a facility management company headquartered in New Delhi. “This leaves MSMEs with little or no cash for further developments and research and development.

“Loan restructuring will definitely boost morale. Due to lack of funds, true Indian potential was not able to come up as the funds rested in the hands of the multinationals.”

Sampad Swain, the chief executive and co-founder of Instamojo, a payment platform for MSMEs says: “This new move by the RBI is a welcome relief, providing solutions to enable business continuity and make for a stable business environment."

In a further step to help the sector, the RBI on Wednesday set up a committee to look at solutions to the financial challenges that small businesses are facing.

“In my view, such moves are necessary as MSMEs form a crucial part of the Indian economy contributing significantly to the country’s GDP,” says Piyush Khaitan, the founder and managing director of NeoGrowth Credit, an SME lending firm in India.

“The biggest challenge that every lending company faces today is to maintain a lower default rate,” he says. “This restructuring policy will benefit the banks and non-banking financial companies as it will also save them from the burden of higher provisioning, further resulting in increased profits.”

Manu Sehgal, the head of business development and strategy at Equifax, a global information solutions company, says small businesses in India have suffered following the twin shocks of demonetisation and GST, combined with a credit squeeze led by the non-banking financial sector after a major shadow bank, IL&FS, headquartered in Mumbai, defaulted on a a series of repayments last year.

The RBI's policy means “small businesses get a grace period for the repayment of their loans, and ... banks do not have to classify those loans as non-performing assets on their books,” says Mr Sehgal.

He says it “may look like” the central bank is giving in to government demands, but points out that the RBI has taken steps before to help small businesses and that a new policy was due.

The RBI's move is “a step towards giving a boost to SMEs sector” given that some small businesses are struggling to repay their debts, says Rajiv Ranjan, the founder and managing director of PaisaDukan.com, a peer-to-peer lending firm based in Mumbai.

He points out the downsides, including a potential negative impact on the credit culture, because some businesses might take advantage of the scheme even though they could have operated perfectly well without it. Other challenges may still persist for such enterprises.

“These companies’ cash flows still remain under pressure,” says Mr Ranjan.

Meanwhile, the RBI is continuing to feel the heat from New Delhi. On Thursday, a parliamentary panel asked the central bank to ease its rules on banks' capital requirements to allow them to increase lending.

But entrepreneurs such as Ms Grover say that for now, they are simply relieved the RBI is taking much-needed steps to help smaller companies.

“I believe he [Mr Das] is doing well for the nation at large,” says Ms Grover. “When it comes to the RBI's independence, only time will tell if it will be preserved or not.”