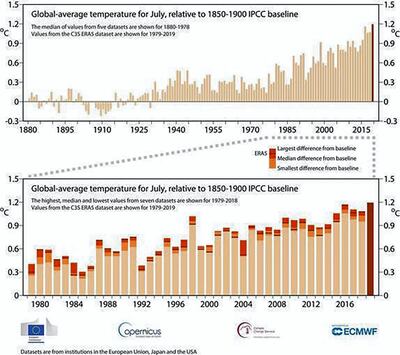

While humans squabble and debate their commitment to combat climate change, nature has been relentless and unforgiving. Extreme weather events are growing in intensity and frequency.

June 2019 was the hottest June in 140 years, setting a global record, and maximum temperatures last seen a century ago were felt in Bagdad, Bahrain and Kuwait. The ongoing drought in India and related acute water shortage continues, threatening rural communities and leading to greater poverty.

Sea levels are expected to rise between 10 and 32 inches or higher by the end of the century. Arctic ice loss has tripled since the 1980s and Antarctica lost as much sea ice in four years - four times the size of France – as the Arctic lost in 34 years. The Global Climate Risk Index reports that “altogether, more than 526,000 people died as a direct result of more than 11,500 extreme weather events; and losses between 1998 and 2017 amounted to around $3.47 trillion (at purchasing power parity rates).

The clear and present danger warning of the 2018 report by the Intergovernmental Panel on Climate Change (IPCC) is going unheeded.

While climate change will be global, its regional impact will be varied and unequal, the Middle East and North Africa (Mena) along with Sub-Saharan countries are among the most vulnerable. Growing desertification, widespread drought, high population growth rates (leading to a doubling of population by 2050), rapid urbanization and extreme heat compound the effects of water scarcity to magnify the impact of climate change. The near absence of climate change combating and risk mitigation policies are aggravating the impact.

The World Bank conservatively estimates that climate-related water scarcity will cost Mena 6 to 14 per cent of its GDP by 2050, if not earlier, while some 17 countries are already below the ‘water poverty line’ set by the UN. The lack of efficient water management infrastructure and policies exacerbate natural water scarcity.

Home to 6 per cent of the global population but just 1 per cent of freshwater resources, Mena will very likely be fighting “water wars” by mid-century. The Tigris and Euphrates rivers are drying up, building up tensions between Turkey, Iraq and Syria over water resources. Ethiopia is building its Grand Renaissance Dam and Egypt claims that it will cut downstream flows and water supply to Egypt by some 25 per cent. The potential for conflict is growing, with Egyptian President el-Sisi openly declaring that the dam is “a matter of life and death”.

Climate change poses an existential challenge, threatening the economic viability of oil-producing countries. The energy transition to comply with COP21 is leading to a global shift away from fossil fuels to greater energy efficiency and renewable energy, implying a secular downward trend in demand for fossil fuels and prices.

The implication is that the main source of wealth and income of the GCC and oil producers could rapidly depreciate in value because of the fall in demand and prices. Fossil fuel asset prices could rapidly deflate leading to “stranded assets” – that is, assets that are not able to meet a viable economic return as a result of unanticipated or premature write-downs. It is estimated that about a third of oil reserves, half of gas reserves and more than 80 per cent of known coal reserves would remain unused in order to meet global temperature targets under the COP21 Agreement.

The “stranded assets effect” would directly impact all economic activities and businesses that extract, distribute and those that use fossil fuels intensively as inputs for production, such as transportation. In turn, the prices of fossil fuel exposed assets (stocks, bonds and financial securities), would rapidly deflate to reflect the growing risks, and loans would become impaired, resulting in a loss to investors, including banks, pension funds, insurance companies and SWFs.

Central banks are raising the alarm that climate risk is a direct financial risk for the banking and financial sector. Mark Carney, Governor of the Bank of England, has highlighted three broad channels through which climate change can affect financial stability. He names physical risks affecting the insurance industry; climate change liability risks due to claims arising from climate change; and transition risks. Transition risks will crop up as changes in policy and technology result in a reassessment of the value of a large range of assets that emerge once they have been stranded. Citigroup forecast that the total value of stranded assets could be over $100 trillion in a 2015 report (based on $70 per barrel of oil, $6.50/MMBTU of gas and $70 per tonne of coal).

The bottom line is that the GCC faces three direct risks from climate change: physical, as heat, rising sea levels and water scarcity become reality; economic, as wealth destruction ensues vast oil reserves becoming stranded assets; and financial, with a banking and financial sector highly dependent and exposed to the oil and gas sector.

What should the GCC countries do? To counter these existential threats, they need to accelerate their economic diversification plans, develop and implement decarbonisation strategies and develop neighbourhood climate risk mitigation policies. The nations have tentatively embarked on this path.

Dr Nasser H Saidi is the chair of the Mena Clean Energy Business Council and founder and president of the economic advisory and business consultancy Nasser Saidi & Associates